Table Of Content

Don’t even consider buying a home before you have an emergency savings account with three to six months of living expenses. When you buy a home, there will be considerable upfront costs, including the down payment and closing costs. You need money put away not only for those costs but also for your emergency fund. You may also be able to take advantage of down payment assistance or closing cost assistance programs as a first-time buyer. Buying a home is still considered a key aspect of the American dream, as a home is typically an appreciating asset that grows in value over time. And you may qualify as a first-time buyer even if you’re not a novice.

Step 4: Decide What Type Of Mortgage Is Right For You

You’ll also need to save money to cover closing costs – the fees you pay to get the loan. Several factors determine how much you’ll pay in closing costs, but it’s best to prepare for 3% – 6% of the loan amount. This means if you’re borrowing $200,000 for your purchase, you might pay $6,000 – $12,000 in closing costs. Your credit score plays a significant role in what loans and interest rates you qualify for. It gives lenders insight into your history of paying your debts on time. Taking steps to improve your credit score and reduce your debt can pay off big as you prepare to apply for a mortgage.

Step 9: Get A Home Inspection

Once you’re seriously shopping for a home, don’t walk into an open house without having an agent (or at least being prepared to throw out the name of someone with whom you’re supposedly working). You can see how it might not work in your best interest to start dealing with a seller’s agent before contacting one of your own. You need to know exactly how much you’re spending every month—and where it’s going. This calculation will tell you how much you can allocate to a mortgage payment. Make sure you account for everything—utilities, food, car maintenance and payments, student debt, clothing, kids’ activities, entertainment, retirement savings, regular savings, and any miscellaneous items. After all, there are so many steps, tasks, and requirements, and you may be anxious about making an expensive mistake.

How Much House Can I Afford?

How To Finance A Mobile Or Manufactured Home - Bankrate.com

How To Finance A Mobile Or Manufactured Home.

Posted: Wed, 06 Dec 2023 08:00:00 GMT [source]

Start touring homes to develop a sense of what you want and don’t want in your home, as well as what type of inventory is available in your desired neighborhood. Once you find a property that meets your needs, work with your agent to negotiate a fair price with the seller. As you’re getting ready to make an offer on a home, it’s important to understand that there is a decent chance that another buyer might not need to submit any kind of pre-approval documentation. Redfin data shows that 16 percent of purchases in the LA metro area were all-cash deals in the first quarter of 2021. While some of those were individuals with big bank accounts, southern California is also home to loads of activity from iBuyers like Offerpad and Opendoor, not to mention local “we buy homes for cash” companies.

If you can’t reach an agreement, you may want to move on and consider other properties. Read over your inspection results with your agent and ask whether they noticed any major red flags. Lenders usually don’t require a home inspection to get a loan, but you should still get an inspection before buying a property. Let’s look at some major expenses related to a home purchase and how much you should save for them. If you’re on payroll, you’ll likely need to provide only recent pay stubs and W-2s. If you’re self-employed or receiving passive income like social security or pensions, you’ll need to submit your tax returns and other documents.

Step 5: Underwriting and closing (30 to 60 days)

Before you even close on the purchase, you’ll need to make sure you have enough money set aside to cover closing costs. These fees will vary by state and by individual transaction, but they will almost certainly range into the thousands of dollars. Come to closing day prepared with your government-issued ID and any requested documents. Bring a cashier’s check for your down payment and be prepared to pay any closing costs.

Step 9: Finalize the closing and move into your house!

Based on the information you have provided, you are eligible to continue your home loan process online with Rocket Mortgage. Use the Rocket Mortgage Home Affordability Calculator to get a rough idea of how much mortgage you can afford. They’ll also want to see a work history (usually about 2 years) to make sure your income source is stable and reliable.

Step 6: Find The Right Real Estate Agent For You

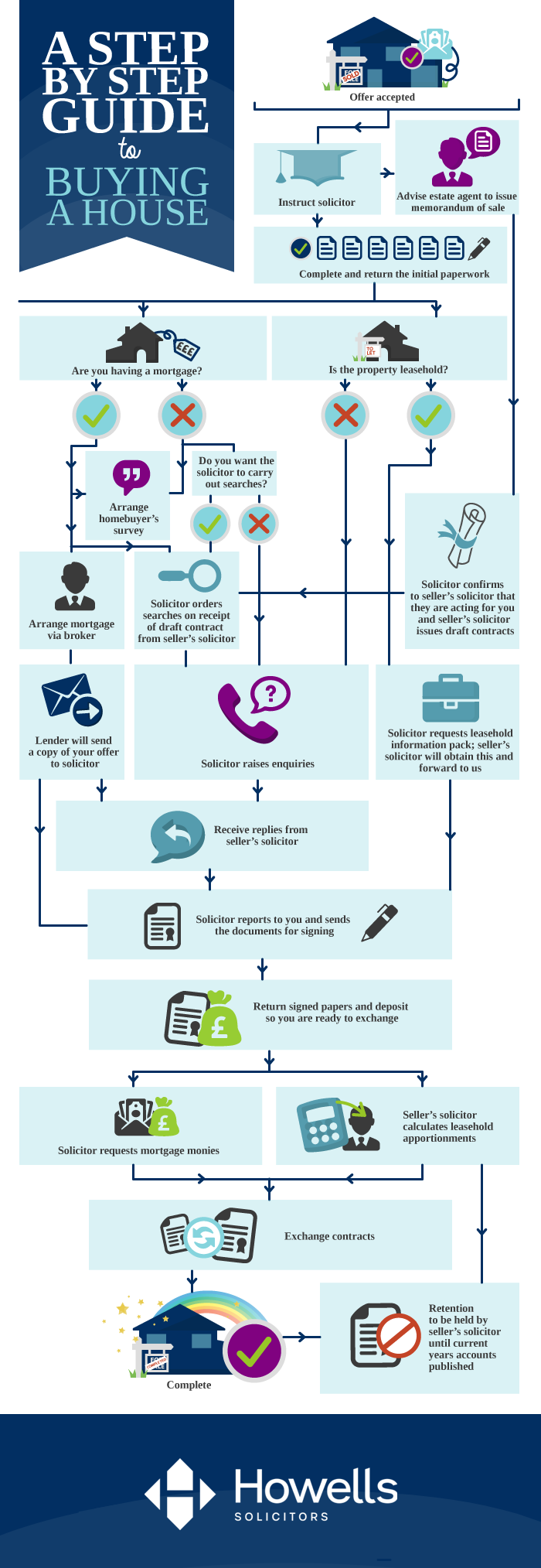

Sometimes a 'factor' is appointed - this is a person responsible for managing and instructing repairs. Tenement properties come with title conditions that apply to all flats - for example, not permitting commercial use. Tenement properties in Scotland include flats in converted houses and high-rise blocks. On the agreed settlement date, the seller will be paid the full purchase price and your solicitor will pay any required Land and Buildings Transaction Tax (LBTT) on your behalf. At this point, the estate agent should removed the property from the market.

Come to the closing

You may also need to have cash reserves to help cover your mortgage in case of emergencies. These reserves are typically equal to at least 2 months’ worth of mortgage payments. Depending on the type of loan you’re applying for and your qualifications, your lender may require more months of payments. In addition to covering a down payment, you’ll need to have enough cash to cover your portion of the closing costs on a home in Los Angeles. Data from ClosingCorp shows that the average closing costs in California added up to 1 percent of the purchase price in 2021.

Keeping in touch with local estate agents could increase your chances of finding your ideal home, as agents sometimes contact registered buyers before listing a property online. Buying a house in cash can streamline the process, but it’s not always the most beneficial decision for a buyer. Depending on how much you have saved up and how much the house costs, you might find yourself strapped later on if you need funds for repairs, maintenance, or to help fund a life event.

So, on a $750,000 home, that’s another $7,500 in expenses before you get the keys. It’s important to note that this figure does not include lender fees, which can add thousands of additional dollars in expenses. Make sure you compare lenders in California to find an option that offers a combination of competitive APR and low fees. When buying a home in California, you’ll likely have to pay for closing costs. These costs include a variety of mortgage-related and third-party fees, and can easily add up to thousands of dollars.

Common counter-offers can include proposed changes to the price, closing date, or purchase contract contingencies. You may go back and forth with the seller a few times before you come to terms you both agree on. Buying a house for the first or even second time can be extremely exciting, but it can also be one of the most complex purchases of your life.

Even if you can’t afford to replace the hideous wallpaper in the bathroom now, you may be willing to live with it for a while in exchange for getting into a place that you can afford. If the home meets your needs in terms of the big things that are difficult to change, such as location and size, then don’t let physical imperfections turn you away. First-time homebuyers should look for a house that they can add value to, as this ensures a bump in equity to help them up the property ladder. This time factor in estimated closing costs (which can total anywhere from 2% to 5% of the purchase price), commuting costs, and any immediate repairs and mandatory appliances you may need before you can move in. Once the seller has accepted the offer, the earnest money will be deposited into an escrow account or held by the listing agent.

No comments:

Post a Comment